![]()

The report provides detailed analysis of both historic and forecast Chinese defense industry values, factors influencing demand, the challenges faced by industry participants, analysis of industry leading companies, and key news. This report offers detailed analysis of the Chinese defense industry with market size forecasts covering the next five years. This report will also analyze factors that influence demand for the industry, key market trends and challenges faced by industry participants.

Over the last few years, China’s defense industry has been cherishing the most productive and lucrative years in its history. The growth of the Chinese Defense industry can be attributed toample state funding, suppressed domestic demand, and access to and development of critical technological know-how on equipment, aircrafts, shipbuilding, missiles etc.

The country’s total defense expenditure during the forecast period i.e. 2016 to 2021 is expected to be USD 1007.1 billion. The average share of capital expenditure is expected to be 32.8% over the forecast period.

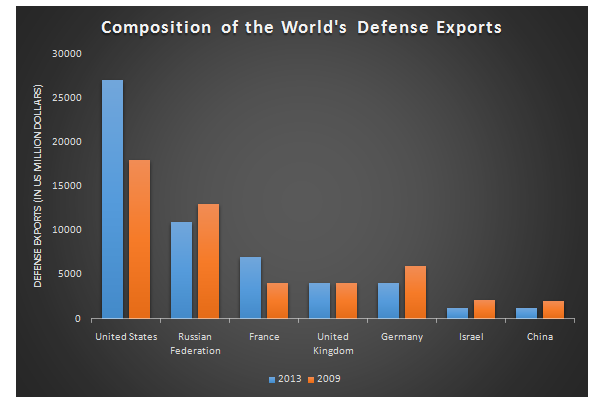

Figure: Composition of the World’s Exports of Defense

While China’s current exports constitute approximately 2.8% of total global defense exports, up from 2.1% in 2009- its total exports are estimated to be just under USD70 billion in 2013-it is clearly very competitive with recognized Western defense exporting nations, such as Spain, Italy, Sweden, and Canada and is closing the gap on Israel, Germany, and the United Kingdom. This improved competitiveness and upward movement in position as a defense exporter is likely to be continued over the next five years and beyond and will, therefore enable China to become a consistent competitor in the global arms market.

China’s export activity has focused primarily on secondary and tertiary defense export markets that are under US or Western export sanctions (Iran, for example) or simply cannot afford or do not need the most expensive Western and Russian platforms and systems. These markets seek to balance “good enough” military technologies with cost, forgiving payment terms and, in a growing number of cases, a strong desire to build or enhance indigenous defense industry through production work-share and technology transfer programs.

On the contention front, the China defense industry is dominated by several large conglomerates including the AVIC Group, China Shipbuilding Industry Corporation, China State Shipbuilding Corporation etc. Two state-owned Chinese firms effectively have joined the ranks of the world’s 10 largest defense companies in a sign of changing military budgets and export markets, according to a new report on the global arms industry. China North Industries Corp. and Aviation Industry Corp. of China sit atop as many as four other domestic producers in the global top 20. China North Industries, better known as Norinco, is the largest of 10 Chinese aerospace and defense holding companies atop a sprawling array of subsidiaries, some of which are listed in Hong Kong.

Key Macroeconomic Trends Expected to Drive Growth of China Defensive Industry

Many factors are predicted to drive China’s Defense Industry, among those increasing military expenditure of China, reducing import reliance, increasing economic growth and rising exports are believed to be the key factors. Some of the remarkable developments of this industry include increasing asset injections, changes in pricing models and management incentives as a part of the SOE reforms, increasing modernization of the PLA. However, the growth of respective industry is hindered by the lower profitability and lack of global competences.The key areas of investment are expected to be fighter and multi-role aircraft, submarines, helicopter, naval vessels, and missile defense systems.

To know more on coverage, click on the link

Related Reports

Contact:

Ken Research

Ankur Gupta, Head Marketing & Communications

+91-124-4230204

{kind=link}